If you’re not famliar with Option Alpha, and are serious about trading options, I highly recommend you check them out! (Disclosure: I’m not affiliated with Option Alpha – just a fan analyzing their publicly available research.)

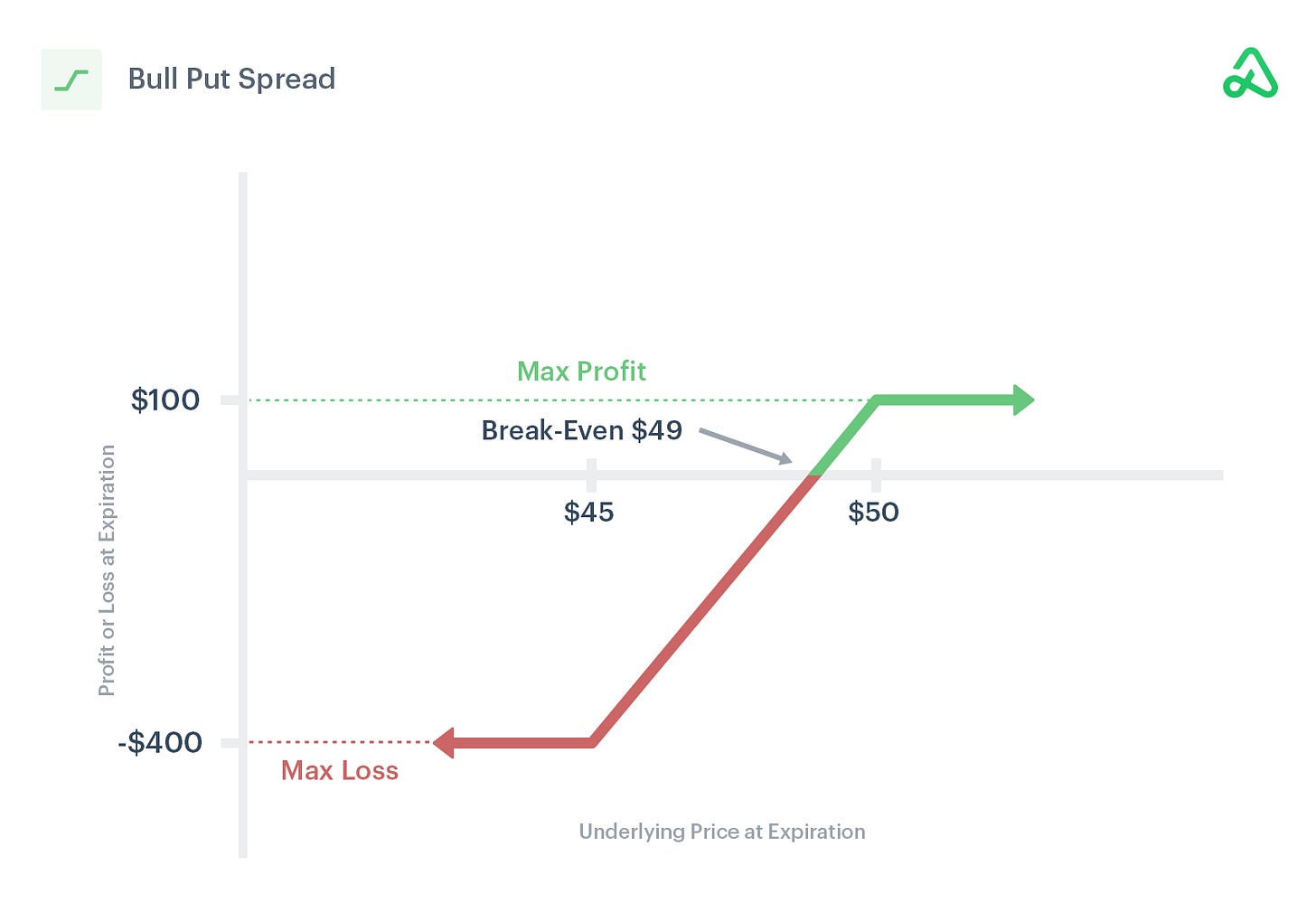

The below shows a risk profile for a sample bull credit spread, selling the $50 strike and buying the $45 strike, for a 4:1 risk:reward ratio.

Their research included extensive backtesting of 0DTE credit spreads across multiple scenarios and timeframes to identify optimal parameters that seem to have captured an edge.

Option Alpha Strategy Performance (July 2022 – July 2025)

- Profit factor: 1.5

- Win rate: 88%

- Return-to-Drawdown ratio: 9x

Given the volatility profile of 0DTE strategies, we’re deliberately not looking at Sharpe ratio. These metrics better capture key 0DTE success factors: consistency and upside potential.

In this post, I set out to achieve similar or better results with their exact parameters – taking them at face value without additional validation. I coded the strategy in Python, using the QuantConnect LEAN framework. Code available further below.

How Daily Liquidity Unlocked this Strategy

This opening range breakout strategy benefits from deep liquidity and predictable market microstructure. When CBOE introduced Tuesday and Thursday SPX expirations in May 2022 – expanding 0DTE options from 3 to 5 days per week – it triggered explosive growth. 0DTE volume surged from 5% to over 40% of SPX options within months.

More importantly, it created more predictable market microstructure. Bank of Canada research documented systematic market maker flows that reduce volatility by 60-90 basis points, creating more reliable and predictable intraday patterns that improve opening range strategy effectiveness.

CBOE’s expansion to daily 0DTE expirations in May 2022 created more predictable market flows that helped make this strategy consistently profitable.

Without further ado, let’s get into the strategy.

The Opening Range: Capturing Early Market Dynamics

The morning trading sessions often establish key price levels as market participants react to overnight developments and establish positions.

The opening trading sessions often set key intraday price levels, as traders digest overnight news and global market developments, and establish positions that shape the day’s trading range.

Option Alpha’s research suggests that the 60-minute range (9:30–10:30 AM EST) provides a superior signal for this strategy compared to shorter 15 or 30-minute periods. Still, different traders define the “opening” window differently, and other periods may be worth exploring.

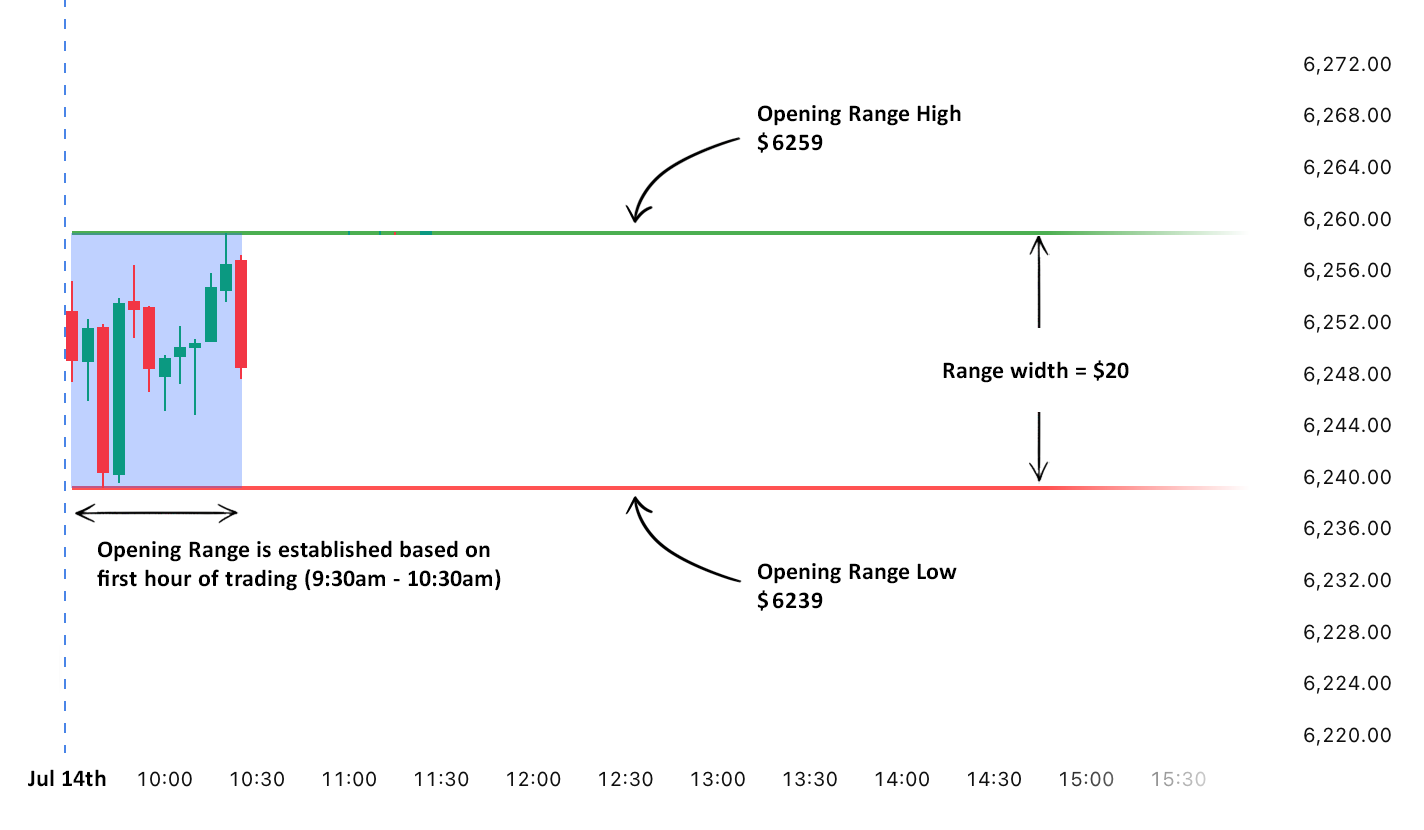

The minimum and maximum prices during the chosen period creates a price range that can act as support and resistance throughout the trading day – provided certain additional criteria are met.

Opening Range Criteria: The 60-minute opening range must be at least 0.2% of the underlying price.

The Morning Setup: Timing Is Everything

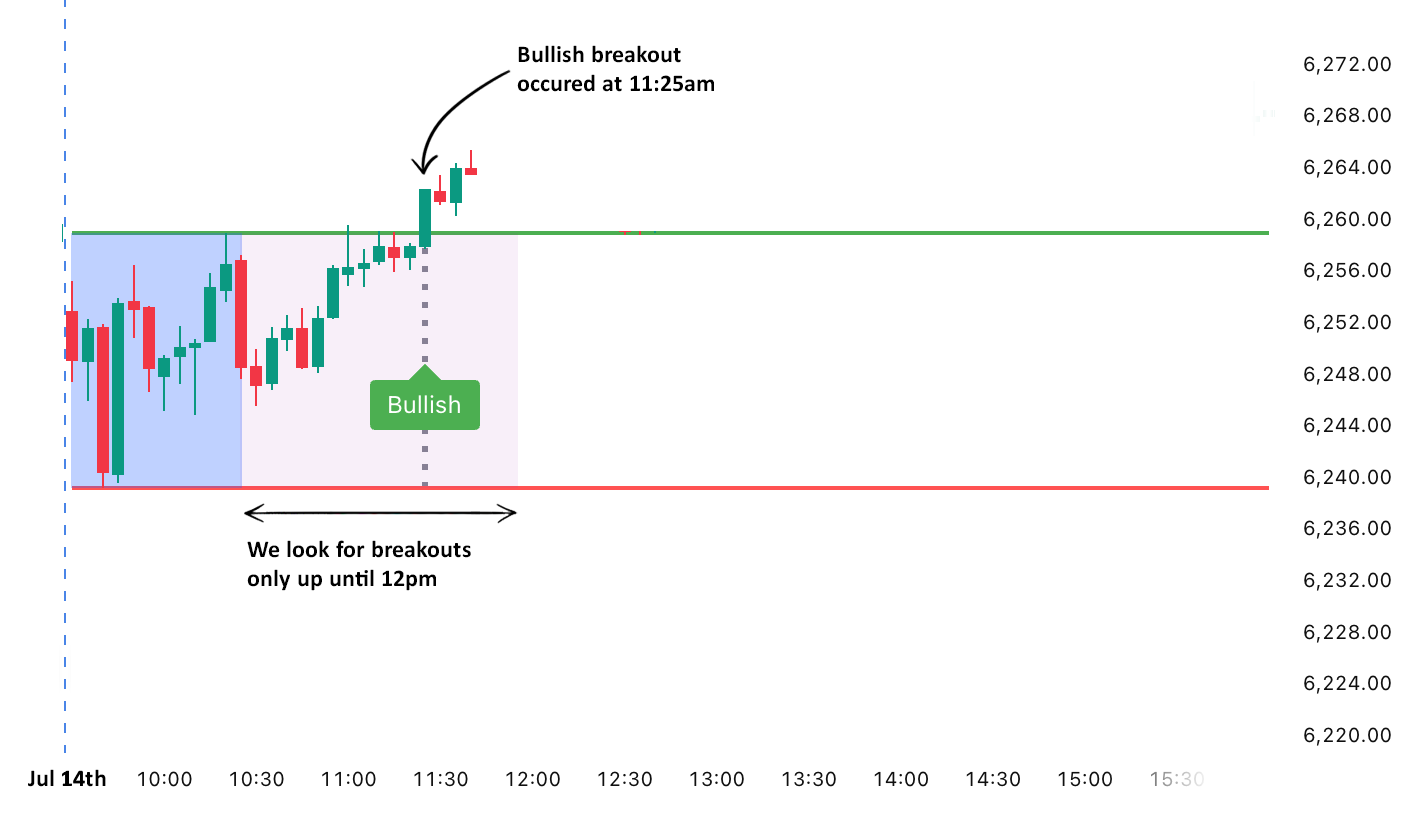

The key opportunity emerges when price breaks outside the established opening range – but timing matters critically. Option Alpha’s backtesting showed entries work best when breakouts occur after range establishment (10:30 AM) but before noon, when sufficient premium and time value remain.

Entry Timing Criteria: Only consider breakouts that occur between 10:30am (when the range is established) and noon.

The Credit Spread Advantage

Here’s why selling credit spreads outperforms buying directional options in this setup:

- Rapid 0DTE theta decay works in our favor

- We don’t need large moves to profit – just staying on the correct side

- We benefit from the tendency of opening range levels to act as support/resistance

- Time decay is our ally rather than our enemy

- Holding till experiation captures the full theta benefit

Exit Criteria: Hold the position till expiration to capture the full theta benefit.

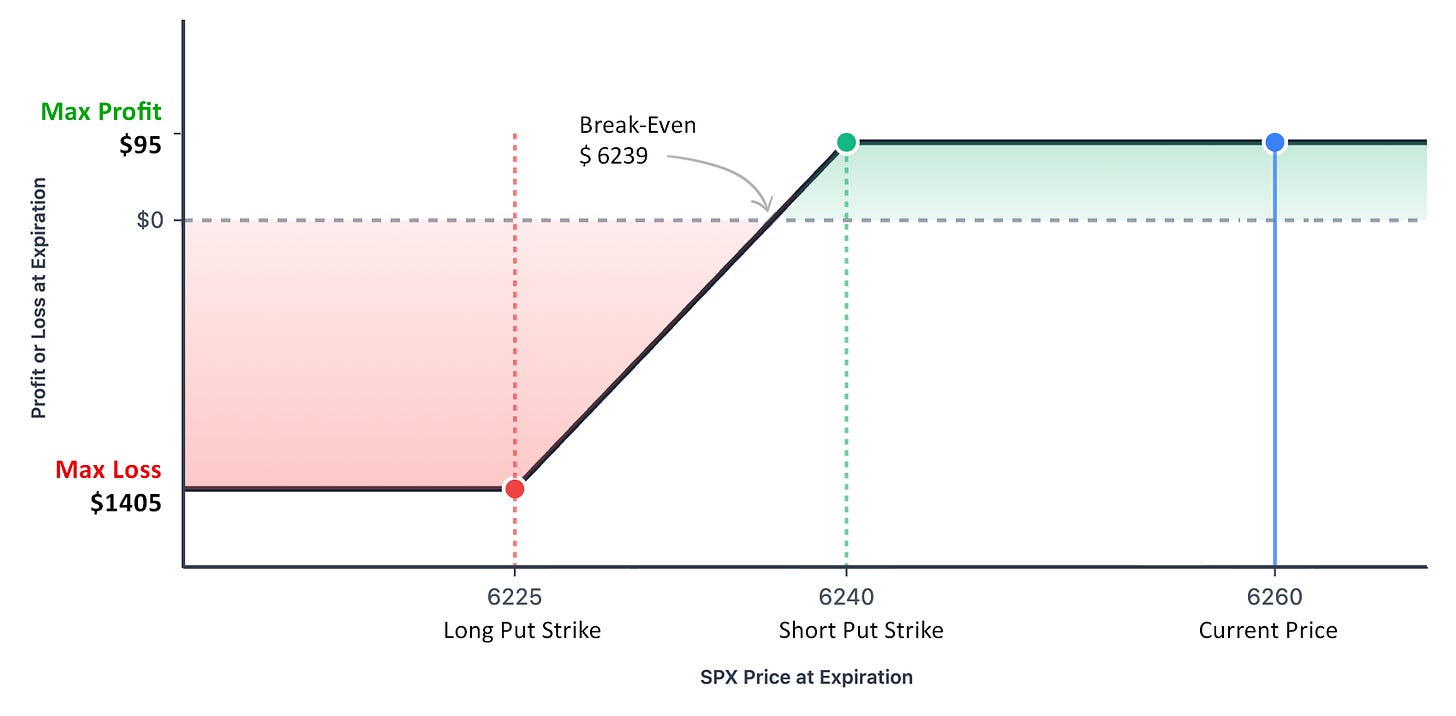

Trading the Breakout: A Successful Bullish Scenario

When SPX breaks above the opening range high, we position for the range low to act as support by selling a put spread.

Real Example from July 14 2025:

- 10:30 AM

- Opening range established: $6239 – $6259

- Range of $20 (~0.32% of price) met minimum range criteria: > 0.2%

- 11:25 AM

- 5min bar closes at $6262, breaking above $6259

- Timing criteria met: breakout occured before noon

- Entry:

- Sell 6240/6225 put spread

- Open a $15 wide spread

- Sell 6240 put (~at range low) for $1.85

- Buy 6225 put (protection) for $0.90

- Collect $.95 credit ($95 per spread)

- 4:30 PM

- Exit:

- Position held till market close (contract expiration)

- Result: Kept the $95 credit – SPX closed at $6268, above our range low

- Exit:

Credit Spread Criteria: The 0DTE credit spread should be $15 wide, with the short leg at the bottom (top) of the range for bullish (bearish) spreads.

Without additional risk management, some trades with this strategy involve extreme asymmetric risk. Such skewed risk-reward ratios only work with very high win rates

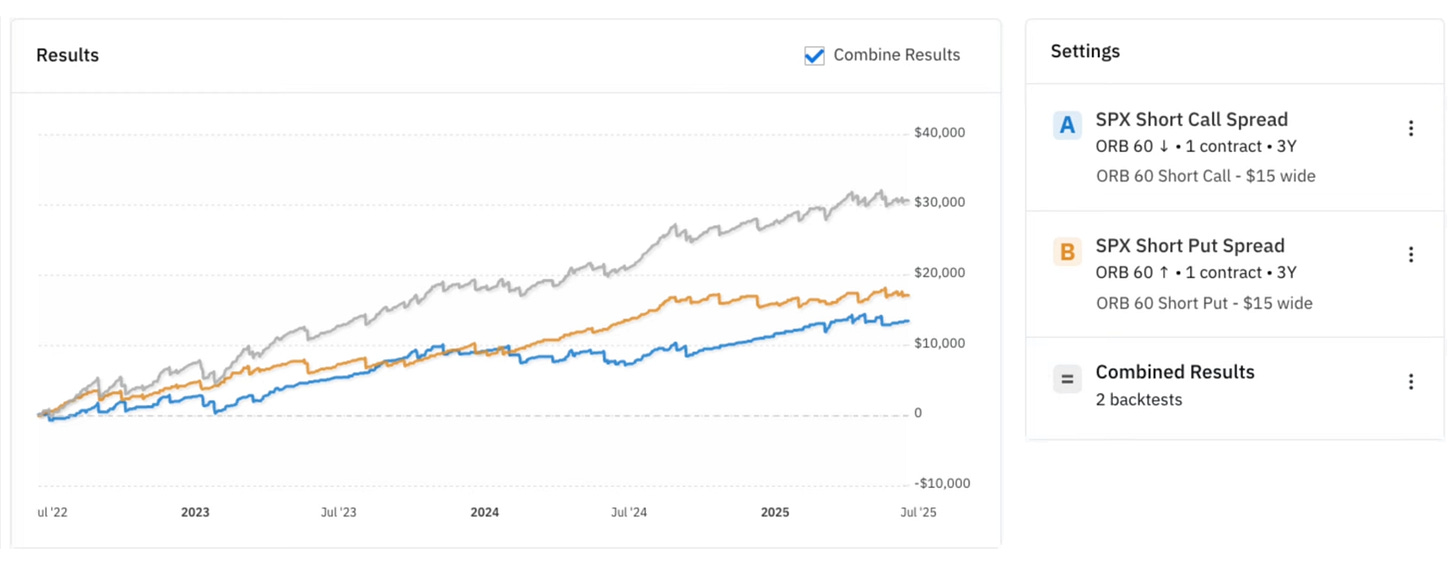

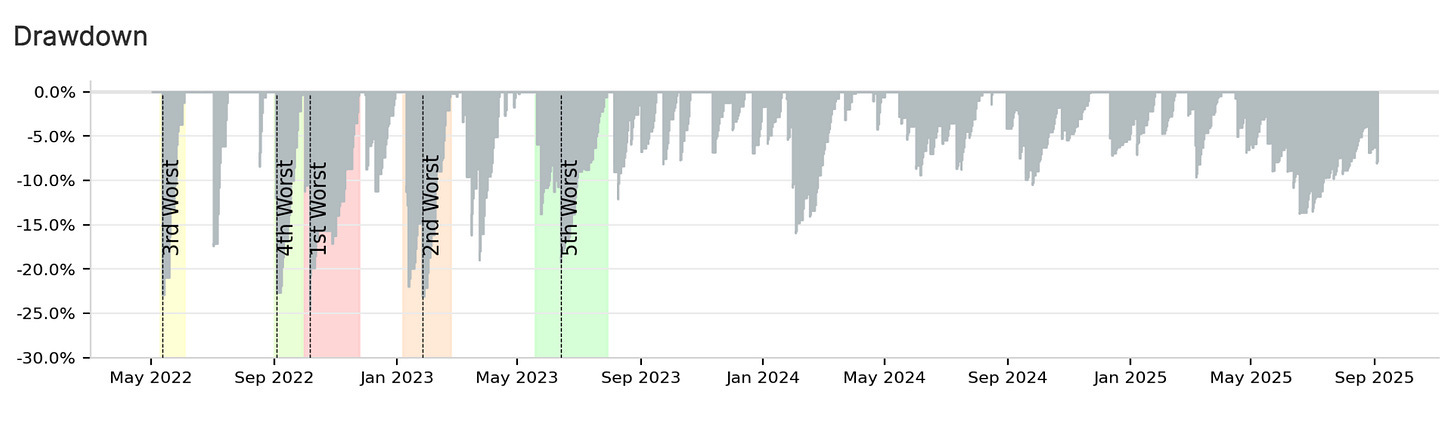

Backtests Results

The following are the results from my backtest of the strategy with a starting balance of $50,000, trading a fixed number of 10 spreads at a time. The equity curves are plotted against a SPY buy+hold benchmark.

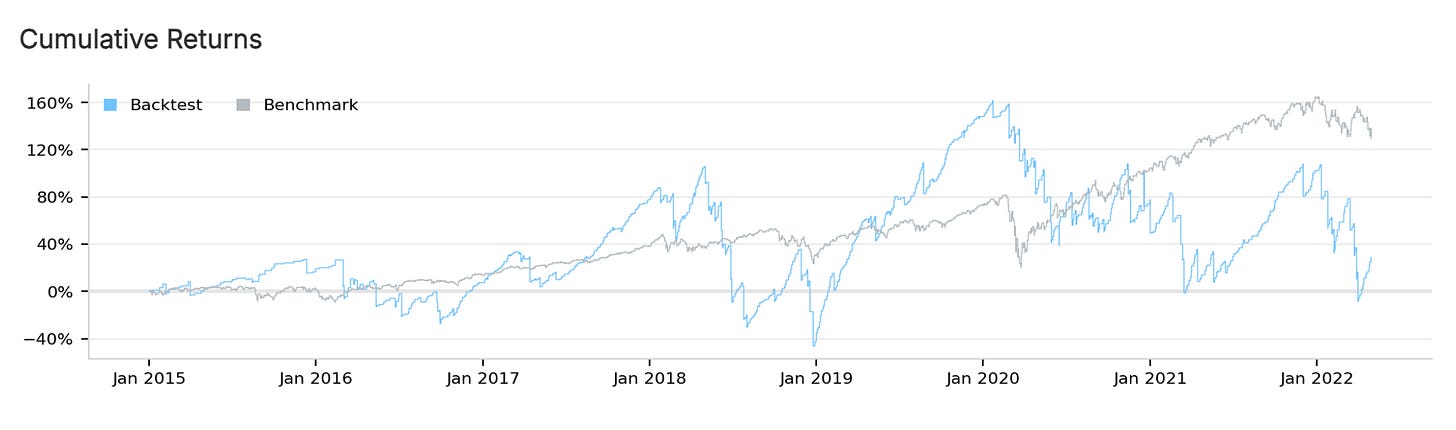

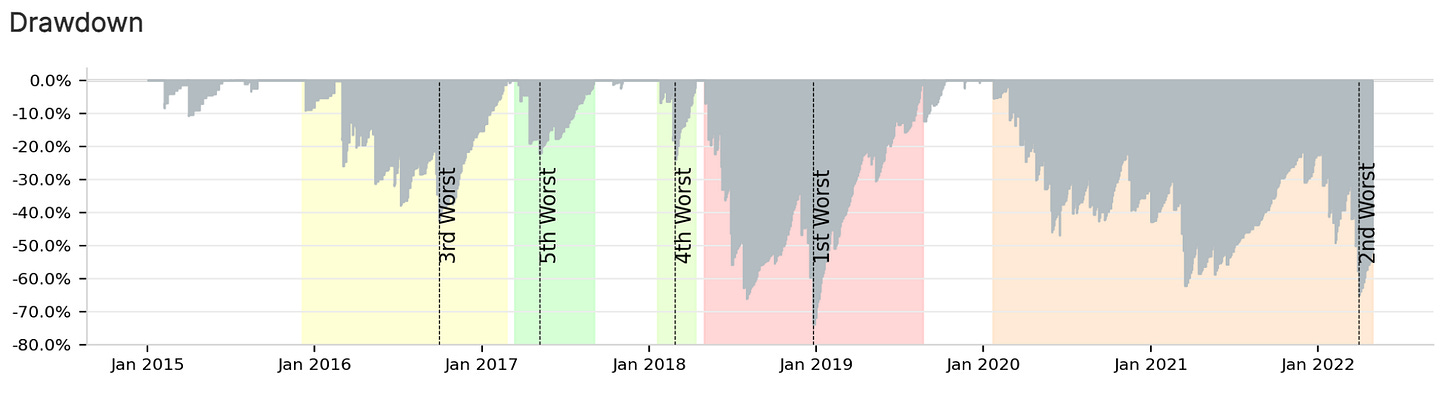

January 2015 – April 2022: Before the CBOE changes

You’ll see that before the CBOE changes, the strategy struggled with inconsistent performance and deep drawdowns due to unpredictable market microstructure and less systematic market maker flows.

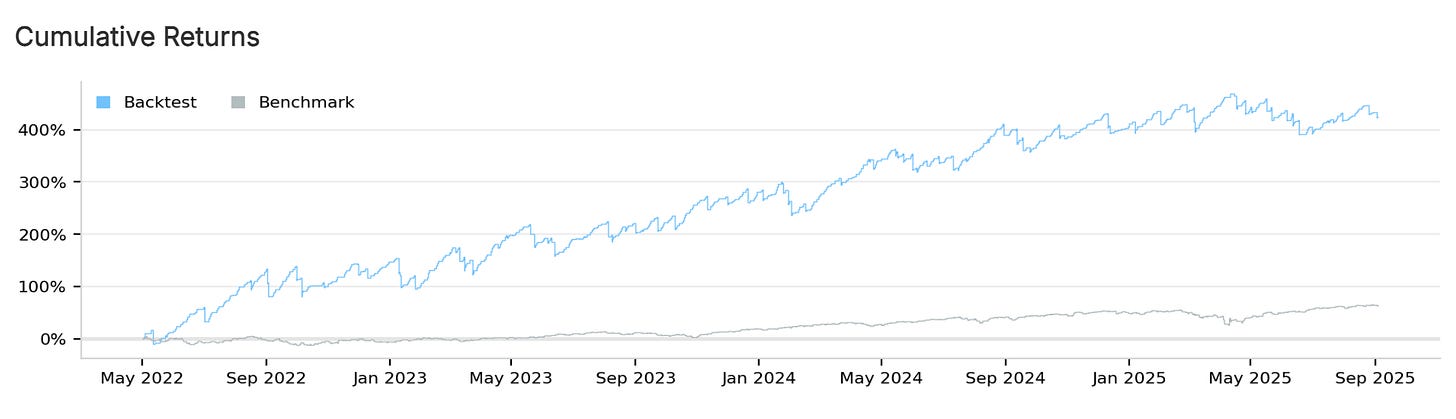

May 2022 – August 2025: After the CBOE changes

Strategy Performance

- Total trades: 661

- Profit factor: 1.3

- Win rate: 86.99%

- Return-to-Drawdown ratio: 17x

Now that’s more like it! The introduction of daily SPX expirations in May 2022 created the ideal environment that this strategy needed to become consistently profitable.

What Made This Edge Possible

- Predictable Gamma Flows

Dealers with positive gamma inventory (typical for balanced 0DTE flow) create systematic mean reversion through delta hedging, strengthening opening range support/resistance. - Non-Linear Theta Decay

Most 0DTE time decay occurs after 3:30 PM ET, creating timing arbitrage for strategies entering during range formation. - Momentum Regime Detection

Opening range breakouts statistically identify transitions from contraction to expansion regimes where dealer flows amplify directional moves. - Enhanced Volatility Concentration

Daily 0DTE availability concentrates 40%+ of SPX volume into single-session expirations, creating amplified intraday volatility patterns that strengthen breakout signals. - Systematic Hedging Predictability

Market makers’ delta hedging of massive 0DTE positions creates mechanical buying/selling flows at key price levels, making opening range support/resistance more reliable than in traditional markets. - Microstructural Timing Advantage

The concentration of gamma exposure and liquidity during morning hours creates optimal conditions for detecting meaningful breakout signals before dealer flows stabilize.

These inefficiencies seem to be optimally exploited using Option Alpha’s identified parameters: a 60-minute window for peak liquidity price discovery, breakouts before noon, and $15-wide spreads (anchored on the range low / high) that provide sufficient credit collection while limiting maximum loss to manageable levels for high-probability trades.

Important Considerations

- Entry Window: Only trade breakouts occurring before noon

- First Breakout Only: Ignore secondary breaks in the opposite direction

- FOMC Exclusion: Skip trading on Federal Reserve meeting days

- Range Validation: Minimum 0.2% range requirement filters weak signals

Research

- Option Alpha’s research walkthrough

- Market microstructure research

- 0DTE gamma dynamics study

- Research on systematic market maker flows

Implementation Resources (strategy code + indicator)

- Interactive Backtest (May 2022 – Aug 2025)

- Click ‘code’ to browse / copy the Pyton code

- Click ‘clone’ to backtest it yourself in Quantconnect

- Note: Some QuantConnect stats dont account for multi-leg options positions properly, so in the interactive report you may see some numbers off, like win rate.

- TradingView Indicator (as seen in screenshots above)

- Add this tradingview indicator to your SPX chart (on intraday timeframes)

- Useful if you’d like to manually trade this.

Future Consideration: A 2025 Reality Check?

Are you interested? Let me know in the comments!